Demand and Supply

Economics Explained, Week 3

Imagine you’re standing in the grocery store and a can of soup is on sale. The store could have offered you “50% off.” Instead, the sign says “Buy One, Get One Free.” Mathematically, those are the same deal. So why do stores almost always pick the second one?

Hold that thought. By the end of this post you’ll know the answer, and you’ll know it because of two of the most powerful ideas in all of economics: demand and supply. They sound boring. They are not. They explain why diamonds cost more than water, why your favorite restaurant raises prices when its rent goes up, and why nobody did anything useful with the steam engine for about 1,600 years.

Let’s start at the beginning.

Substitutes and Complements: The Things Around the Thing

Economics has a simple way to sort the goods in your life. Some things are “or” goods:

If you’re hungry, you could eat pizza or a salad.

If you’re looking for a date night activity, you could go to the movies or go play putt putt.

If you’re looking for a place to live, you could rent or you could buy a house.

You pick one when the other gets too expensive. Those are substitutes.

Other things are “and” goods:

Hot dogs and buns.

A mouse and a keyboard.

Dinner and a baby-sitter (if you have kids).

You tend to buy them together, and when the price of either one rises, you end up buying less of both. Those are complements.

One word, “or” versus “and,” and you’ve already got a working map of how prices ripple through your shopping cart.

Why does this matter? Because the price of one good never stays contained. It reaches into everything connected to it, boosting the “or” goods and dragging down the “and” goods. Keep that in mind as we build out the rest of the picture.

The Puzzle That Stumped Economists for 250 Years

Here’s a question that made some very smart people look very silly for a very long time.

Which is more valuable, water or diamonds?

If I offered you a gallon of water or a gallon of diamonds (that’s about 29 pounds of diamonds), which would you grab? The diamonds, obviously. But that’s strange, isn’t it? Water keeps you alive. Diamonds just sit there and sparkle. The thing that’s essential is nearly free, and the thing that’s useless for survival costs a fortune.

This was called the water-diamond paradox, and it genuinely puzzled economists for centuries. Everybody knew it was true. Nobody could explain why.

The answer arrived in the 1860s and 1870s, worked out independently by William Stanley Jevons, Léon Walras, and above all Carl Menger, the founder of the Austrian school, who nailed it most cleanly. Their insight has a clunky name, “marginal analysis,” but a simple idea behind it.

“Marginal” just means the next one. Not all the water in the world versus all the diamonds in the world. Just the next gallon of each.

And there’s the trick. Water is everywhere, so the next gallon is worth almost nothing to you. You can get it from the tap. Diamonds are rare, so the next one is worth a great deal. Think about how easy it is to go fetch a gallon of water versus a gallon of diamonds.

So we have to separate two things people constantly mix up:

Use value: what the thing does for you. Water keeps you alive; diamonds look pretty.

Exchange value: what you can get for it in trade. Here diamonds win in a landslide.

The paradox dissolves the moment you stop thinking in terms of “all or nothing” and start thinking at the margin.

This isn’t just a parlor trick about jewelry, by the way. It’s how to think about your whole life. Your textbook might frame it as “studying for an exam versus keeping a friend,” as if you had to choose one or the other. But you don’t. Real decisions are almost never all-or-nothing. You don’t choose between all studying and all friendship. You choose how to spend the next hour. Anyone who tells you that you must sacrifice the entire friendship to pass the test isn’t much of a friend, and isn’t much of an economist either.

This is why I get twitchy whenever a politician starts talking about “needs.” Framing things as “needs” pushes you straight into all-or-nothing thinking. People do have needs. But in a world of scarcity, there are always trade-offs at the margin, and pretending otherwise is how bad policy gets sold.

The Demand Curve, Demystified

Once you accept scarcity, demand falls right out of it. Demand simply relates how much of something people want to the sacrifice they have to make to get it. In plain English: it relates the price to how much you buy.

Would you buy more of something when the price is low, or when it’s high? Low, of course. Draw that on a graph with price going up the side and quantity going across the bottom, and you get a line that slopes downward. Higher price, less bought. Lower price, more bought.

Now, one distinction that trips up nearly everyone, and it’s worth getting right:

Demand is the whole line, the entire relationship between every possible price and how much you’d buy at each.

Quantity demanded is a single point on that line, the specific amount you’d buy at one specific price.

Keep those straight and you’ll already understand price better than most people who write about it for a living.

This gives us the Law of Demand: hold everything else constant, raise the price, and the quantity demanded falls. Lower the price, and quantity demanded rises. That’s it. It’s why you stock up when something is on sale.

Here’s the part people get backwards constantly: a sale does not “increase demand.” The whole line didn’t move. You just slid down to a different point on the same line. The price dropped, so the quantity demanded went up. Saying “the lower price increased demand” is like saying stepping on the scale made you heavier. Worth being precise about, because once the line itself starts moving, you’ll want to know the difference.

Why does the line slope down in the first place? Diminishing marginal utility, that same idea from the water and diamonds. The first slice of pizza is glorious. The fourth is fine. The seventh you’re forcing down out of spite. Each additional unit is worth less to you, so you’ll only buy more if the price drops to match.

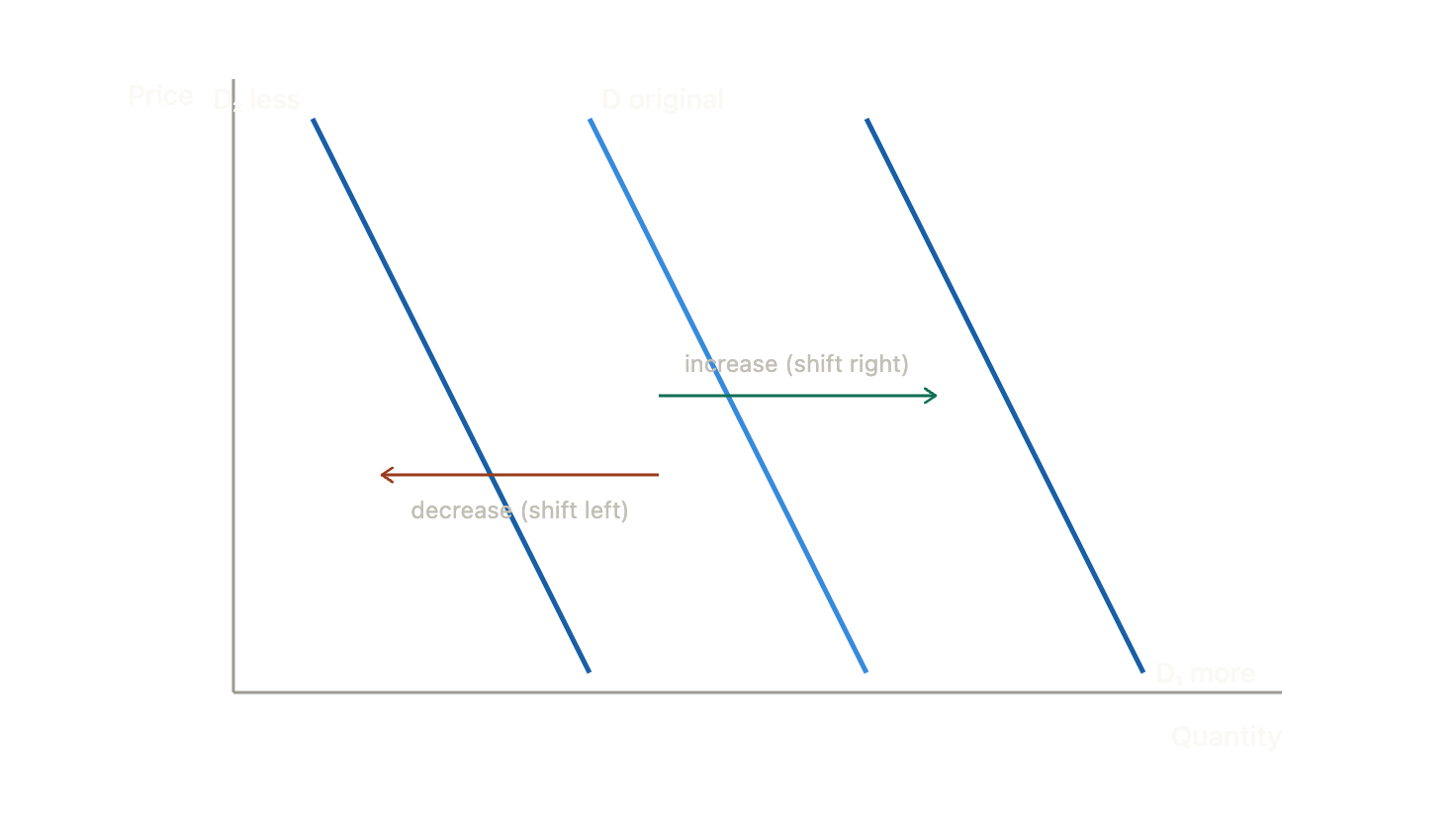

When the Whole Line Moves

The demand curve itself can shift. When it slides right, people want more at every price. When it slides left, they want less at every price. Here’s what that looks like:

Notice the difference from a sale. A sale keeps you on the same line and slides you down it. A shift picks up the entire line and moves it. Six things move it:

The number of buyers. More people who want the product means more sold at every price. The line shifts right. Fewer buyers, it shifts left. Simple as that.

Tastes and preferences. You just decide you like something more or less. Imagine you woke up tomorrow and your favorite food made you gag. You’d buy a lot less of it at any price. Or someone learns how animals are treated before slaughter and swears off meat for good. Their demand curve for steak collapses leftward, no price change required.

The price of a substitute. Here’s where the neighbors come in. Go-karting, mini golf, and the movies all make decent dates. If go-karts and mini golf get expensive, the movies start looking better, and demand for movie tickets shifts right. (Though notice: with date night getting pricier overall, you’ll probably go on fewer dates altogether. Can you see why?)

The price of a complement. Drop the price of one thing and you’ll want more of its partner. Cheaper kegs mean more demand for red Solo cups. Cheaper printers mean more demand for ink. The two travel together.

The expected future price. If you think the price is about to jump, you buy more today. This is perfectly ordinary. You stock up before a storm. You buy the car before the tariff hits. You fill the tank when you hear gas is going up next week. Expectations move the line right now, before the future even arrives.

Income. This one splits in two. A normal good is something you buy more of as you get richer: restaurant meals, vacations, new cars. An inferior good is something you buy less of as you get richer. The classic example is boxed mac and cheese. Broke college students eat a mountain of it, and there’s nothing wrong with that, it’s a sensible response to a thin budget. But once the paychecks get bigger, most people trade up. They don’t quit mac and cheese forever, they just eat less of it. New cars instead of used. Craft beer instead of whatever’s cheapest. Same person, different income, different choices.

Put it all together and you reach a slightly dizzying conclusion: the demand for anything depends on the demand for everything else. The price of kegs touches the market for cups. Your raise touches the market for mac and cheese. It’s all connected. Which is exactly why economists lean on the phrase ceteris paribus, Latin for “all other things held constant.” We freeze the rest of the world so we can study one thing at a time. We know the world doesn’t actually hold still. We’re just not magicians.

Now, the Other Half: Supply

Demand is about the people who want the stuff. Supply is about the people who make it. And supply runs on an idea you already know in your bones: opportunity cost.

Of course factories buy raw materials. No surprise there. But here’s the part that’s easy to miss. The factory has to convince the seller of those materials to sell to them rather than to anyone else on Earth. Why does that matter?

Because resources have opportunity costs too. When you use a chunk of titanium to make a golf club, that same titanium can’t become an airplane part. So when a business buys materials, it’s effectively making a bold claim: “I can turn this titanium into something more valuable than anyone else on the planet can, which is why I’m willing to outbid them all for it.”

And here’s the beautiful part. The only way that business survives is if it’s right. If it can’t actually produce something more valuable than its competitors with those materials, it loses money, it fails, and it stops gobbling up resources that someone else could use better. Profit and loss aren’t just scoreboards. They’re a sorting mechanism that pulls resources toward whoever uses them best and yanks them away from whoever doesn’t. Isn’t that something?

This is where the difference between accounting profit and economic profit earns its keep:

Accounting profit is just dollars in minus dollars out. Revenue minus expenses.

Economic profit is accounting profit minus opportunity cost, what you gave up to do this instead of the next best thing.

Suppose I have two job offers. A professorship that pays $200,000, or a job at McDonald’s that pays $35,000.

Taking the McDonald’s job isn’t “free.” It costs me the $200,000 professorship I turned down, which is why its economic profit is deeply negative. The accountant says I made $35,000. The economist says I lit $165,000 on fire. Both are right. They’re just answering different questions, and the economist’s question is usually the one that matters for decisions.

Why the Supply Curve Slopes Up

The supply curve slopes upward, the mirror image of demand, and it captures increasing marginal cost.

Picture yourself stranded on an island, Tom Hanks in Cast Away, spending all day catching fish. Now you want some coconuts. Which fishing spot do you abandon first, your best or your worst? The worst, naturally. And which coconut tree do you climb first? The best one. Want more coconuts? Now you give up your second-best fishing spot for your second-best coconut tree. And the third. And the fourth.

Every step, you sacrifice more fish to get fewer coconuts. That’s increasing marginal cost, and it’s exactly why the supply curve rises. The more you produce, the more valuable the alternatives you have to give up.

You feel this in your own life. How much harder will you work for $1,000 than for $1? To pull more hours out of you, I have to pay enough to outweigh whatever you’d give up. Lay out a typical day, sleep, gym, friends, TV, video games, eating, reading, and rank it by what you’d hate to lose. Ask you to work two hours and you’ll skip the gym, the thing you value least. Cheap. Ask for eight hours and now I’m taking your reading, your games, time with friends. That hurts, so I’d better pay a lot more. The supply curve is that rising price you demand as I ask you to give up more and more valuable pieces of your day.

And once again, mind the distinction:

Supply is the whole line, the producer’s willingness to produce across all prices.

Quantity supplied is the single amount actually produced at one given price.

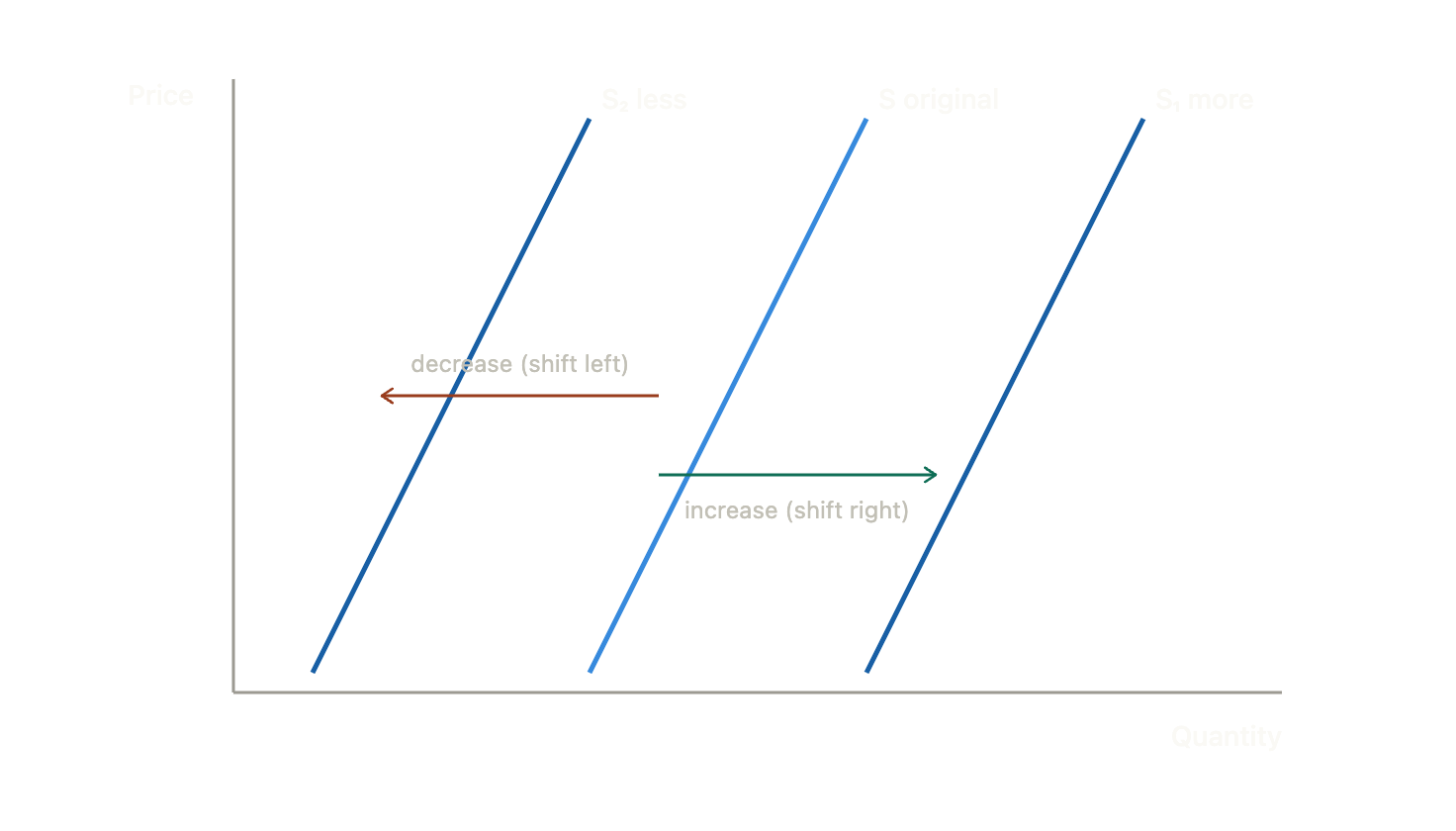

What Makes the Supply Line Move

Just like demand, the whole supply curve can shift. Right means more produced at every price; left means less:

Four big movers push it one way or the other:

The price of resources. If steel gets more expensive, Ford’s willingness to crank out cars drops. Supply shifts left. Cheaper inputs shift it right.

Technology. When Eli Whitney’s cotton gin made it dramatically easier to process cotton, the supply of cotton products exploded rightward. Most technology shocks push this way, and here’s a humbling thought about how fragile that progress is. Hero of Alexandria built a working steam device, the aeolipile, back in the first century AD. And then nothing. For roughly 1,600 years it sat there as a toy and a temple parlor trick until Thomas Savery built a practical steam pump in 1698, and then Newcomen and Watt turned it into the engine of the Industrial Revolution. The idea was right there the whole time. Sometimes the bottleneck isn’t the invention. It’s everything around it.

Nature and political disruption. A hurricane wrecks the local supply curve, shifting it hard left. So do “political storms.” When a brutal dictator seizes power, people are understandably afraid to show up to work, and supply shifts left. Elect leaders who get the incentives right and you can shift it the other way. What exactly those good policies are is a longer argument for another day.

Taxes. And here I want to be careful, because this is a positive statement about how the world works, not a normative one about what we should do. Raise the cost of producing something, through a tax, and businesses produce less of it. Supply shifts left. Lower that cost and they produce more. Supply shifts right. That’s just the mechanics.

Now, please don’t go charging out of here yelling “the economist said cut all business taxes!” Because I didn’t. Tax dollars fund roads, courts, defense, and plenty else, and whether and how much to tax is a genuine normative debate worth having. All I’m telling you is what the supply curve does when you pull the tax lever. What you should do with that lever is up to you and the ballot box. My job is to make sure that when you step into that voting booth, you at least know which way the lever moves things. That’s education. The rest is your call.

So, BOGO or 50% Off?

Back to the grocery store. Why “Buy One, Get One Free” instead of “50% off,” when the math is identical?

Because demand slopes down.

Say each can of soup sits on the shelf for $1.50. To you, the first can is worth $2, but the second is only worth 50 cents, because of diminishing marginal utility. That second can just isn’t worth as much to you as the first.

Run the 50% off deal and each can costs you 75 cents. You happily buy the first can (worth $2 to you, a steal at 75 cents). But the second? It’s only worth 50 cents to you, and they want 75 cents for it. No sale. You walk out with one can, the store collects 75 cents, and it just gave away margin on the can you would’ve paid full price for anyway.

Now run BOGO. You pay $1.50 and walk out with two cans. The first was worth $2 to you, so you’re thrilled. The second was only worth 50 cents, but hey, it was “free,” so why not. The store collects $1.50 instead of 75 cents and moves twice the inventory.

Same math on the sign. Wildly different outcome at the register. The store isn’t being sneaky, it’s reading your demand curve and pricing the second can, the one you value less, at the only price you’d ever pay for it: zero. Everybody walks away happy, which is sort of the whole magic of trade.

The Big Idea

Strip away the jargon and here’s what demand and supply really teach you. Value isn’t fixed and it isn’t found in the thing itself. It lives at the margin, in the next unit, in the next hour, in the next trade. Water versus diamonds, your job versus the one you turned down, the first can of soup versus the second, it’s all the same lesson. There’s no “all or nothing.” There’s only “what’s the next step worth, and what does it cost?”

Get comfortable thinking that way and the world stops looking like a series of moral absolutes and starts looking like what it is: a vast web of people making trade-offs, bidding for resources, and signaling to one another through prices what they value and what they don’t. No one’s in charge of it. And it works remarkably well anyway.

That’s not a reason to cheer for any particular policy. It’s a reason to understand the machine before you start yanking its levers.